Retirement in Canada can be thrilling and intimidating as your vibrant career winds down. Envision the freedom to explore new passions, travel the world, or take a well-deserved break. The possibilities are endless; retirement is a time to look forward to with anticipation and excitement. But how can you turn these dreams into reality without financial stress?

It’s not just about saving money; it’s about crafting a blueprint for a comfortable, worry-free retirement. Mastering the art of strategic retirement saving and planning is not just essential; it’s empowering. It puts you in control of your future.

Dive deeply into our guide and uncover vital strategies to ensure a retirement that fulfills your aspirations and financial objectives. Following a well-crafted retirement plan will bring a sense of accomplishment and peace of mind. Your future self will thank you!

Saving For Retirement in Canada

Adapting Your Retirement Plan: Navigating Change and Timing

Retirement in Canada is evolving, and your plan may need updates to align with current realities. Increased life expectancy, shifting family dynamics, and unexpected costs can impact retirement goals.

As personal circumstances change, it’s crucial to reassess and adjust your plans to ensure they meet your current needs and expectations. Your goals from 10 or 20 years ago might no longer fit, and that’s okay. Adjusting your plan to reflect these changes will help you stay on track.

There’s no perfect age to retire, but the most important thing is getting ready for a retirement that can adjust to your needs. It’s helpful to start talking with your family and advisor early to navigate these changes and maximize your retirement years.

Planning Your Retirement Income: How Much Is Enough?

Determining how much you need for retirement in Canada requires careful consideration and strategic planning. Here’s a guide to help you calculate the correct amount:

Evaluate Your Future Spending:

Consider how your expenses will change. While you reduce work-related expenses and commuting costs, you could increase spending on hobbies, travel, or home renovations. Tailor your savings to accommodate these changes.

Understand Income Replacement Needs:

A standard recommendation is to aim for 60–70% of your current income during retirement. However, this varies depending on your financial situation. Lower-income retirees may need to maintain their current income level, while higher earners require less.

Factors in Inflation:

Inflation will erode the purchasing power of your savings over time. Plan for rising costs by estimating future expenses using tools like the Canadian Retirement Income Calculator, and adjust your savings to keep pace with inflation.

Plan Your Retirement Age:

The timing of your retirement significantly impacts how much you need to save. Early retirement means you’ll need to cover more years of expenses without income. Aim to save enough to sustain yourself for a potentially lengthy retirement period.

Account for personal circumstances:

Your retirement plan should reflect your situation, including debt, family support, and whether you plan to relocate. If you are retiring abroad, be aware of different regulations and costs that may affect your finances.

By addressing these factors and planning accordingly, you can ensure that you have the necessary funds to enjoy a comfortable and secure retirement in Canada.

Retirement Income Options in Canada

In Canada, you have three primary sources of retirement income:

Government Benefits:

- The Canada Pension Plan (CPP) provides monthly payments based on your work contributions.

- Old Age Security (OAS): Monthly payments for seniors aged 65 and older, adjusted for inflation.

- Guaranteed Income Supplement (GIS): Additional support for low-income seniors receiving OAS.

Employer Pensions:

- Defined Benefit Plans: Guarantee a specific monthly payout.

- Defined Contribution Plans: The payout depends on contributions and investment returns.

- Locked-In Retirement Accounts (IRAs): These accounts are designed to retain pension funds from previous employment. They are ‘locked-in’ because they restrict when and how you can withdraw the funds, usually to ensure they are used for retirement purposes.

Personal Investments and Savings:

- Registered Retirement Savings Plan (RRSP): Tax-deferred savings, taxed upon withdrawal.

- Tax-Free Savings Account (TFSA): Tax-free investment growth and withdrawals.

- Registered Retirement Income Fund (RRIF): Convert RRSPs to periodic withdrawals, taxed as income.

- Annuities: Provide guaranteed payments for a specified period or lifetime.

- Personal Savings and Investments: This category includes many options, from traditional savings accounts to more complex investments like bonds and stocks. Considering a mix of these options is essential to ensure a diverse and effective retirement income strategy.

- Pension Income Splitting: This strategy allows couples to reduce their tax liability by splitting pension income. It can be a valuable tool for managing taxes in retirement, but it’s essential to understand the rules and limitations before implementing this strategy.

- These options can be combined to create a diverse and effective retirement income strategy.

Maximizing Your Retirement Savings

Effective Withdrawal:

- Strategize RRSP withdrawals and consider converting to RRIF.

- Explore tax-efficient withdrawal strategies and LIRA options.

Continued Growth:

- Invest in growth options like segregated funds or annuities.

- Ensure your retirement savings include investment opportunities.

Part-Time Work:

- Consider turning hobbies into income sources.

- Retirement is a chance to pursue interests and supplement income.

Budgeting:

- Create a new budget reflecting changes in income and expenses.

- Anticipate increased costs (utilities, travel) and savings (transportation, taxes).

Spousal Planning:

- Align retirement goals and investments with your partner.

- Discuss estate planning and retirement timing together.

Health and Wellness:

- Focus on health with more time for exercise and activities.

- Consider lifestyle changes for improved well-being.

Evolving Financial Needs with Age

Healthcare Costs:

- Younger Years: Healthcare expenses are generally lower, with a focus on preventive care and occasional medical visits.

- Older age: increased likelihood of chronic conditions and need for frequent medical or long-term care. Health insurance and savings for medical expenses have become more critical.

Income Needs:

- Younger Years: A higher income needs to support work-related expenses, housing costs, and raising children.

- Retirement Age: Reduced income needs as work-related expenses decrease. However, you may need additional funds for travel, hobbies, or lifestyle changes.

Housing Costs:

- Younger Years: Larger housing expenses, including mortgages and property taxes. Potentially higher utility and maintenance costs.

- Older Age: Potential for downsizing to a smaller home or condo, reducing housing expenses. Some may consider moving to retirement communities or assisted living.

Work-Related Expenses:

- Younger Years: Higher costs associated with commuting, professional attire, and career development.

- Retirement Age: Significant reduction or elimination of these expenses as you retire.

Debt and financial obligations:

- Younger Years: Often higher levels of debt, such as student loans, mortgages, or car loans.

- Older Age: Focus shifts to managing or eliminating remaining debt, including mortgages or loans, to reduce financial strain in retirement.

Savings and Investments:

- Younger Years: Focus on building savings and investments, contributing to retirement accounts, and accumulating assets.

- Older Age: Emphasis on drawing from savings, managing investments to provide steady income, and planning for the longevity of assets.

Family Responsibilities:

- Younger Years: Supporting children, education expenses, and helping aging parents.

- Older Age: shifting the focus to supporting grandchildren or planning for inheritance and possibly facing the need to assist with family members’ health care.

Lifestyle and Leisure:

- Younger Years: Spending on career development, family activities, and more significant expenses.

- Older Age: increased spending on leisure activities, hobbies, travel, and potentially more focus on enjoying retirement.

Understanding these changes can help you plan and adjust your financial strategy throughout different stages of life.

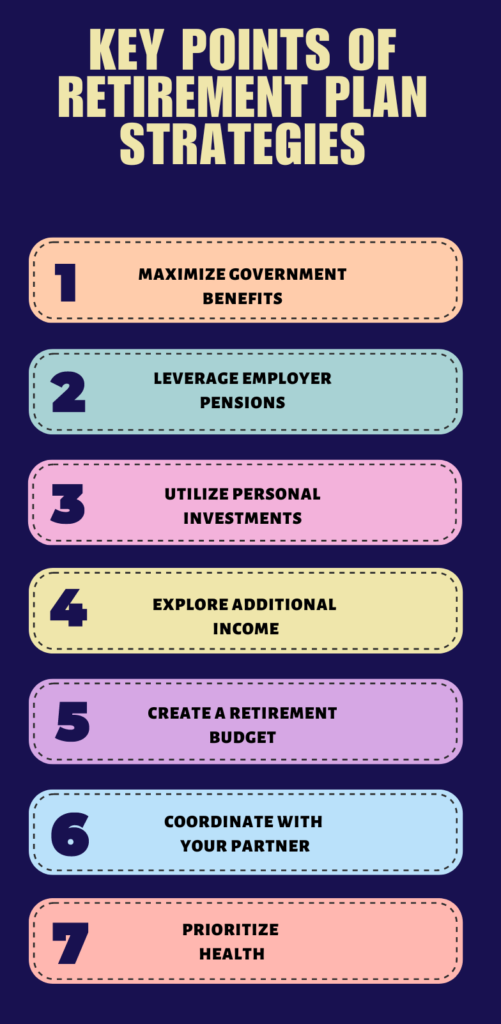

Critical Points of Retirement Plan Strategies in Canada

Maximize Government Benefits: Optimize CPP, OAS, and GIS for full advantages.

Leverage Employer Pensions: Review and manage defined benefit and contribution plans.

Utilize Personal Investments: Manage RRSPs and TFSAs and consider annuities for steady income.

Explore Additional Income: Consider part-time work and continue investing.

Create a Retirement Budget: Adjust for new expenses and maintain a detailed budget.

Coordinate with your partner: Align retirement goals and plan for estate needs.

Prioritize health: Stay active and consider lifestyle adjustments for well-being.

Enjoy the journey!!

As you finalize your retirement plans with your advisor, remember that this is an exciting new chapter. While finalizing financial details is crucial, remember that retirement is your time to explore your passions, savor new experiences, and genuinely enjoy life. Embrace this new chapter with excitement and anticipation—your best years are beginning. It’s a chance to focus on what you’ve put aside during your working years. Embrace retirement as an opportunity to enjoy everything you’ve always wanted.

FAQ- Retirement in Canada

How do Canadians plan for retirement?

For most people, their retirement income will come from these four sources: Personal savings and investments. Employer-sponsored pension plans. Canada Pension Plan (CPP) or Quebec Pension Plan (QPP)

What is the best retirement strategy?

A 401(k) plan is one of the best ways to save for retirement, and if you can get bonus “match” money from your employer, you can save even more quickly. A 401(k) plan is one of the best ways to save for retirement, and if you can get bonus “match” money from your employer, you can save even more quickly.

What is a good monthly income for retirement in Canada?

According to Statistics Canada’s 2024 Canadian Income Survey, the average after-tax retirement income for senior families in 2022 was $74,200, or $6,183 per month. For individual seniors, it was $33,600, or $2,800 per month.

How do I minimize taxes in retirement in Canada?

Five ways to pay less tax in retirement

Contribute to a spousal Registered Retirement Savings Plan (RRSP) …

Split pension income with your spouse/common-law partner.

Withdraw your assets in the right order.

Have extra assets? …

Keep contributing to your Tax-Free Savings Account (TFSA)

How much money is needed to retire comfortably in Canada?

According to this rule, you’ll need 70% of your pre-retirement household income each year in retirement for 25 years. For example, if your household brings in $150,000 in the year before you retire, then you’ll need $105,000 annually. Multiply that by 25 years, and your retirement savings goal would be $2,625,000.

How many years do you have to work in Canada to get a pension?

Your employment history is not a factor in determining eligibility. You can receive the Old Age Security (OAS) pension even if you have never worked or are still working. If you are living in Canada, you must be 65 years old or older.